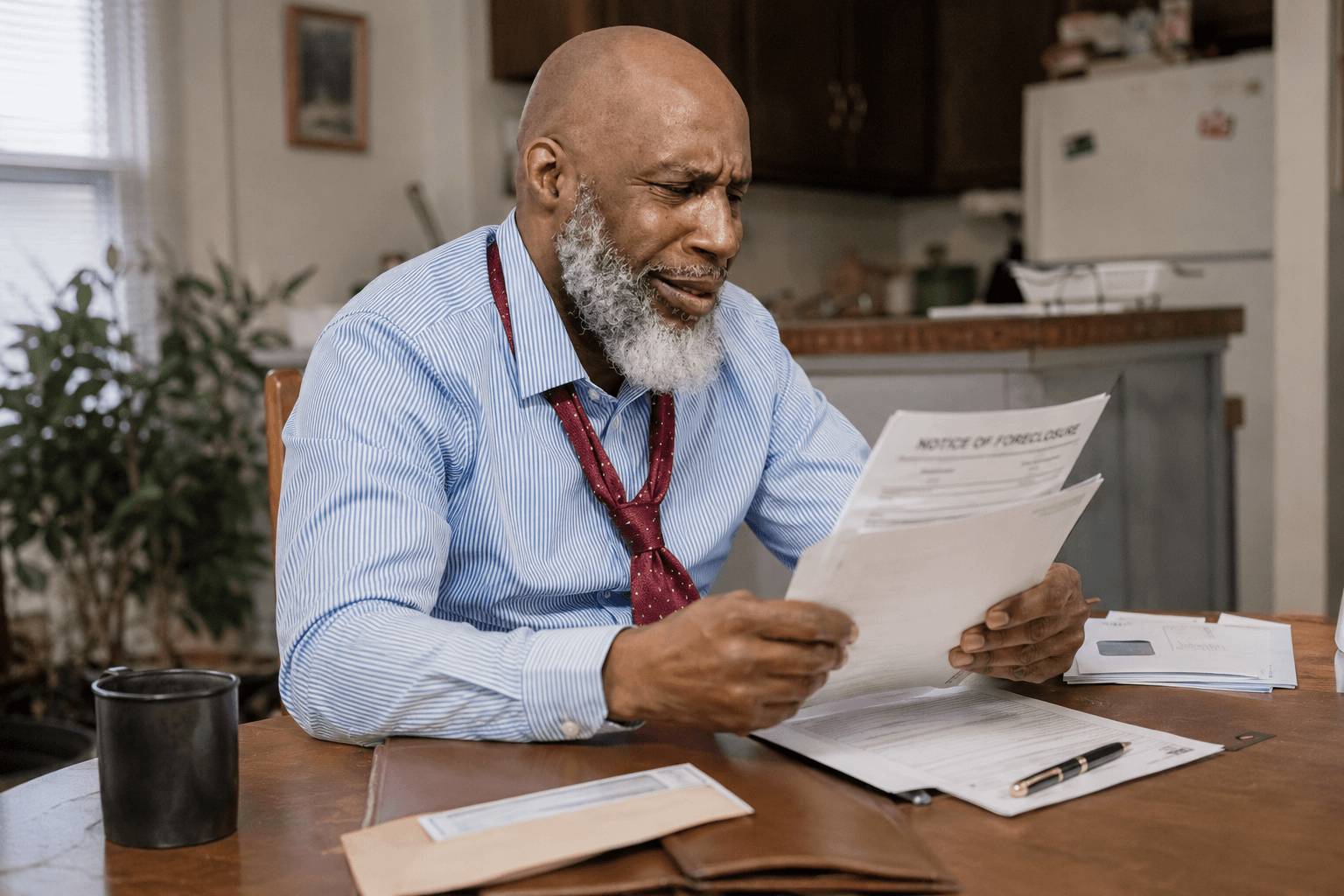

Receiving a foreclosure notice is one of the most stressful things a homeowner can face. The clock starts ticking the moment the process begins, and without a clear plan, you can end up losing your home and your equity. The good news is that in most cases, you have more options—and more time—than you might think.

Here’s what you need to know about selling your house before foreclosure is finalized in Kansas City, and why acting sooner rather than later makes a significant difference.

The information below is for general educational purposes only and is not legal advice. If you are facing foreclosure, we strongly recommend consulting with a HUD-approved housing counselor and a licensed real estate attorney who can advise on your specific situation.

How Foreclosure Works in Missouri

Missouri is a non-judicial foreclosure state, which means lenders can foreclose without going through the court system. The process moves faster here than in states that require a court judgment.

The general sequence: (Missouri RSMo. § 443.310 — Power of Sale)

- First missed payment — Your lender will begin outreach and late notices typically within 30 days.

- Continued default — After several months of missed payments, the lender moves toward formal action. The window varies by lender and loan type.

- Notice of default / acceleration — The lender formally declares the loan in default and may accelerate the balance, meaning the full loan amount becomes due.

- Publication — Missouri law requires the foreclosure sale to be advertised in a local newspaper for a set period before the sale can occur.

- Trustee’s sale — The property is auctioned to the highest bidder. Once this sale occurs, you lose both the property and any remaining equity.

The overall window from first missed payment to trustee’s sale in Missouri is often in the range of 4–8 months, though it can be shorter in some circumstances. (RSMo. § 443.310)

Right of redemption in Missouri: Missouri has very limited post-sale redemption rights in most residential foreclosure situations. In practice, once the trustee’s sale occurs, reclaiming the property is rarely a realistic option—which is one reason acting before the sale date matters so much in Missouri. (RSMo. § 443.350)

How Foreclosure Works in Kansas

Kansas uses a judicial foreclosure process, meaning foreclosures go through the court system. This generally makes the process longer than Missouri’s non-judicial path.

The general sequence: In many cases the window is 3 to 12 months depending on your equity and circumstances — an attorney can tell you which applies to you.

- The lender files a lawsuit in district court after a period of default.

- The homeowner is served with a summons and has an opportunity to respond.

- If the court rules in the lender’s favor—typical in a genuine default—a judgment is entered and a sheriff’s sale is scheduled.

- The property is sold at a court-supervised sheriff’s sale.

Because of the court process involved, the overall timeline in Kansas is generally longer than Missouri—sometimes a year or more from first missed payment to sale. (K.S.A. § 60-2401 et seq.)

Right of redemption in Kansas: Kansas law provides homeowners with a redemption period after the sheriff’s sale in certain circumstances, during which the homeowner may be able to reclaim the property by paying the full amount owed. The length and conditions of the redemption period depend on the type of property and the specific circumstances of the foreclosure. (Kansas K.S.A. § 60-2414 — the redemption window is in many cases 3 to 12 months depending on your equity and circumstances — an attorney can tell you which applies)

Kansas vs. Missouri in practical terms: If your home is on the Kansas side of the metro, you likely have more time to act than a Missouri homeowner in the same situation. That said, waiting on that extra time is rarely a good strategy—costs and credit damage accumulate regardless of which state you’re in.

Options Before Foreclosure

You have more choices than foreclosure or doing nothing. Here’s an honest look at the main options, with realistic tradeoffs for each.

Reinstatement

If you’ve missed payments but can catch up in full—including missed payments, interest, late fees, and any legal costs—reinstatement brings your loan current and stops the foreclosure process. This is the cleanest option if it’s financially possible. Contact your lender directly to get a reinstatement quote and understand the deadline by which it must be paid.

Loan modification or forbearance

Lenders sometimes agree to modify the terms of your loan—a lower interest rate, extended term, or principal forbearance—to make payments manageable again, or to grant a temporary forbearance period. Not all borrowers or loans qualify, and lender approval is required. The earlier you contact your lender, the more likely these options are available. Waiting until a sale date is scheduled dramatically narrows what’s on the table.

Short sale

If you owe more than the home is currently worth, a short sale—where the lender agrees to accept less than the full payoff balance—may be an option. Short sales require lender approval, take significant time to process, and aren’t guaranteed. They’re best pursued early in the foreclosure process. A short sale also has credit consequences, though typically less severe than a completed foreclosure.

Deed in lieu of foreclosure

A deed in lieu is an agreement where you voluntarily transfer ownership of the property to the lender in exchange for the lender canceling the debt and stopping the foreclosure. Not all lenders will accept one, and it still has credit consequences. The potential benefit is a negotiated resolution that lets you move on faster and with somewhat less damage than a completed foreclosure.

Selling before the sale date

If you have equity in the property—meaning the home is worth more than you owe—selling before the foreclosure sale is often the best financial outcome available. A sale lets you pay off the mortgage, keep any remaining equity, and avoid a foreclosure on your credit record. A traditional MLS listing takes 45–90 days from listing to close. A cash sale can typically close in as little as two weeks (most in 3–4 weeks), which is often the only path that works within a tight timeline. Learn more about how we work with Kansas City sellers facing this situation.

If you owe more than the property is worth, a sale alone may not fully resolve the debt. You’d need to either negotiate a short sale or cover the difference at closing. Knowing your equity position before exploring a sale is essential.

Bankruptcy

Filing for bankruptcy can temporarily stop a foreclosure through an automatic stay, buying time to reorganize finances or complete a sale. This is a complex area with significant long-term implications and is best pursued only with the guidance of a licensed bankruptcy attorney.

What to Do Right Now If You Are Behind on Payments

Contact your lender immediately. Lenders have loss mitigation departments specifically to work with borrowers in default. Call them. Ask what options are available, what the current status of your loan is, and what your reinstatement amount would be. This conversation is less difficult than most people expect, and waiting only closes doors.

Understand your foreclosure timeline. Get the sale date in writing if one has been scheduled. Every decision you make works backward from that date.

Get a payoff statement from your lender. This tells you exactly how much a sale would need to cover. Without this number, you can’t make a clear-eyed decision about any of your options.

Get a realistic property valuation. Not what you hope the house is worth—what a buyer would actually pay for it today, in its current condition. A local real estate agent or cash buyer can give you a market-based number quickly, usually without cost or obligation.

Talk to a HUD-approved housing counselor. HUD-approved counselors provide free foreclosure prevention counseling and can help you understand your options and navigate lender conversations. You can find local Kansas City-area agencies through HUD.gov’s housing counselor locator. This is a free resource staffed by people who deal with these situations every day.

Consult a real estate attorney if you have legal questions. Especially for Kansas homeowners with questions about redemption rights, anyone considering a short sale or deed in lieu, or anyone dealing with a complex title situation—legal guidance is worth the investment.

Frequently Asked Questions

Can I sell my house if I am behind on mortgage payments in Kansas City?

Yes—as long as the foreclosure sale hasn’t occurred, you still own the property and have the right to sell it. The proceeds from the sale pay off the mortgage first. If there’s equity remaining after the payoff and closing costs, you keep it. If you owe more than the property is worth, you’d need to either negotiate a short sale or cover the difference at closing.

How fast can I sell before a foreclosure sale in Missouri?

A cash sale can typically close in as little as two weeks (most in 3–4 weeks) from an accepted offer, assuming title is clear. This makes it the most reliable option when the foreclosure sale date is close. A traditional listing takes 45–90 days from listing to close—possible if you have enough runway, but risky if your timeline is tight. The most important step is knowing your exact sale date so you can understand which paths are realistically available.

Will selling before foreclosure hurt my credit less than a foreclosure?

Generally, yes. A completed foreclosure is one of the more damaging events on a credit report and can affect your ability to obtain financing for several years. Selling before foreclosure—or completing a short sale—typically has less severe and shorter-lasting credit consequences, though any missed payments will have already had some impact.

What if I owe more than my house is worth?

This is called being underwater on your mortgage. Your main options are: negotiate a short sale (requires lender approval), pursue a loan modification to make the home affordable long-term, consider a deed in lieu of foreclosure, or consult a bankruptcy attorney about your options.

Can a cash buyer help me avoid foreclosure?

If you have equity in the property and the sale proceeds will cover your mortgage payoff, yes—a cash sale that closes before the foreclosure sale date achieves the same result as any other sale, just faster. If you’re underwater, a cash buyer alone doesn’t solve the shortfall. You’d still need your lender to agree to accept less than full payoff through a short sale process.

How Hearthstone Properties KC Can Help

We work with Kansas City homeowners in pre-foreclosure situations regularly. We can give you a fair cash offer on your home as-is—no repairs, no showings, no delays—and close on a timeline that works within your foreclosure window. We can also walk through a traditional listing with you if that makes more financial sense given your specific situation.

There’s no obligation. The goal is to help you understand your options clearly so you can make the decision that’s right for you.

Schedule a quick call and we’ll take a look at your situation together. Time matters in a foreclosure situation. See exactly how we work with Kansas City sellers — from first contact to closing — so you know what to expect at every step.

Who you’ll be working with: When you contact Hearthstone Properties KC, you’re talking directly with Chris Hudson — the owner. Not a call center, not an acquisition manager. Chris is a licensed Kansas REALTOR® with 30+ local deals closed in the Kansas City area. He’ll walk through your specific situation personally and give you an honest answer on whether selling to Hearthstone makes sense for you.

Related: Kansas foreclosure redemption rights — what homeowners need to know | Cash offer vs. listing with a Realtor — see both options side by side

If you’re facing foreclosure on a property in south Kansas City — including Harrisonville, Belton, or Grandview — the process and your options are the same, and time is equally critical. The earlier you reach out, the more paths remain open.

If you’re behind on a mortgage in eastern Jackson County — Blue Springs, Independence, or Lee’s Summit — the process and your options are the same. Time is the variable that matters most.

If you’re facing foreclosure on a property in south Kansas City — including Harrisonville, Belton, or Raymore — the process and your options are the same, and time is equally critical.

The foreclosure timeline also applies in south KC suburbs — Belton, Grandview, and surrounding Cass County communities. The same urgency applies anywhere in the metro.

Ready to Stop the Foreclosure Clock?

Chris responds within minutes — not hours. No obligation, ever.